![]()

Good news for property buyers, but even better news for property developers and sellers.

The affordability ceiling of a first-time buyer who qualifies for a Government FLISP subsidy has been increased from the previous average home loan amount of R 680 000.00 to a value of up to R 870 000.00.

This is a significant property price increase of R 190 000.00; and may change the property industry for first-time buyers and property sellers.

This “price jump” means that sellers will have an abundance of buyers for their properties in a market that is currently under strain.

More people can afford to buy their own homes instead of a never-ending cycle of renting.

Further good news is that a property priced under R1 million is also exempt from transfer duty, as per the recent budget speech announcement.

HOW ON EARTH AND WHEN DID THIS HAPPEN?

No changes were implemented to increase the FLISP subsidy amounts, but the outcome as demonstrated below is a welcome relief for the property sector.

There are two reasons for this “price jump”,

The Interest rate adjustment.

The recent 1 % drop in the prime lending rate. This means that on an income of R18 000 per month, a home buyer can qualify for R41 750 more property finance with the new prime interest rate of 8.75% compared to the previous 9.75% interest rate.

The Banks are competing for business and coming to the “party”. They are adjusting the RTI or “Repayment To Income” ratio.

I was blown over recently to learn that two of the financial institutions active in the home loan market were able to bend over backwards to improve their RTI criteria – repayment to income ratio offering and increased their usual income ratio of 30% to 35%.

This was for a home loan applicant with a very good credit score and sufficient affordability”, says Meyer de Waal of MDW INC Attorneys, who assist home buyers with FLISP and home loan applications.

De Waal went on further to explain this phenomenon,

We received a FLISP application for a home loan of R 800 000 already approved by a Bank.

The first check is to establish the gross income of the applicant. The maximum income for a FLISP application is R 22 000.00.

Based on past experience, the maximum home loan a buyer with an income of R22 000 would obtain would be a home loan of +/- R 680 000.

The R 800 000 approval raised alarm bells.

I immediately contacted our home loan originator Chantelle to question the income of the buyer as it will be fruitless to submit a FLISP application if the buyer earns more than R 22 000 per month.

I learned from Chantelle that a home loan for R 800 000 was approved for a client who earns R 19 700 per month.

I asked her: “How did this happen- did the bank make a mistake?”

Chantelle Wallace, a mortgage origination consultant with My Bond Fitness, went on to state,

The financial institutions are looking for exceptional clients.

At the moment I am aware that two home loan lenders are prepared to bend over backwards for clients who have a good credit score and can demonstrate sufficient surplus, or in banking terms, “repayment to income value”.

“Sufficient surplus or repayment to income ratio“ means that the home loan applicant does not have too much debt to service every month and will have a sufficient surplus left of his or her salary after paying the new home loan, living expenses and debt repayment.

In this instance, the bank was willing to extend the usual 30 % ratio of repayment and offered a 35 % RTI.

This increase meant that the home buyer was granted a higher home loan amount and this increased his buying power.

Not every home buyer will qualify for this exceptional home loan offer, and we urge home buyers to educate themselves a bit more how to prepare and groom yourself for a home loan application, before you take the big step to buy a property and apply for a home loan.

CONSUMERS ARE STILL TRAPPED IN DEBT

Although financial institutions are keen to approve home loans, still some 56% of home loans are still declined.

The average South African citizen spends almost 66% of his or her income to service debt.

“We have taken hands with mortgage origination companies to assist their clients who were unsuccessful to raise a home loan to lend a helping hand to improve the budget management and as such improve affordability and credit profiles for future home buyers.

We also structured a budget fitness programme for clients who sign up for a rent to buy home ownership programme. The Rent2buy programme is available in the price range R400 000 – R1,8 million.

Many FLISP first time buyers will also qualify for a Rent2buy purchase opportunity.

We assist the rent to buy clients to stay budget fit and increase their affordability and improve their chances to qualify for a home loan approval at the end of a 2-year rent to buy cycle,” says Paul Slot of Octogen.

For more information on the Rent2buy Finance and Debt Repair process – click here to watch a video.

EVEN BETTER NEWS FOR FIRST TIME BUYERS

The even better news for a first-time buyer is that such buyers can qualify for a FLISP Government subsidy.

To qualify for this subsidy, a home buyer must:

1. be a South African citizen;

2. earn between R3 501– R22 000 (do not have a gross combined household income of more than R 22 000);

3. be a first-time buyer with a dependent, such being a spouse or a child;

4. have an approved home loan;

5. the buyer must never have had the benefit of a housing subsidy before.

As an example: the home buyer with an income of R 19 700 per month ought to qualify for a FLISP subsidy of R39 408.00.

To calculate a FLISP subsidy – click here on the FLISP Subsidy Calculator.

HOW TO APPLY THE SUBSIDY

The FLISP subsidy can be used in many ways:

1. Improve your own buying power.

Add the R39 408.00 to the home loan of R 800 000 and buy a property of R 839 408.00

2. Pay your transfer and bond costs – (only available in the Western Cape).

In the Western Cape a buyer can use the FLISP subsidy to pay transfer and bond costs. Transfer and bond costs on a purchase price of R 800 000 and a similar bond amount will be R 21 500.00 for transfer costs; and R 20 300.00 for bond costs. Use this handy transfer and bond costs calculator.

3. Reduce your home loan amount and save thousands over your home loan repayment term.

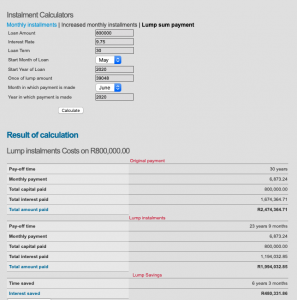

3.1. If a subsidy of R 39 048.00 is paid back into the bond as a “once-off” payment, a further R 480 331.00 can be saved over the 30-year term it takes to repay a home loan. This is close to 50 % of the home loan and 6 years and 3 months can be shaved off the home loan repayment;

3.2. We however would urge the client to pay back the home loan faster; and this can be calculated as follows, says De Waal:

IT IS NOW THE TIME TO BUY YOUR OWN PROPERTY

WHAT SHAPE ARE YOU IN FOR THE BEST HOME LOAN DEAL?

DO YOUR OWN FITNESS TEST TO SEE IF YOU ARE READY TO QUALIFY FOR THE BEST HOME LOAN RATE

Go to FLISP Credit Score Check to determine if you are ready to qualify for the best home loan deal – complete your credit score online and also do your online affordability calculation.

“The recent reduction of 1 % in the interest rate as well as the aggressive competition between the financial institutions created the ideal time for a first-time buyer to get his or her foot on the property ladder,” says De Waal.

Meyer de Waal